The Coming Era of Pension Poverty

Assuming “growth” will fund all promised pensions and entitlements is magical thinking.

The core problem with pension plans is that the promises were issued without regard for the revenues needed to pay the promises. Lulled by 60 years of global growth since 1945, those in charge of entitlements and publicly funded pensions assumed that “growth”–of GDP, tax revenues, employment and everything else–would always rise faster than the costs of the promised pensions and entitlements.

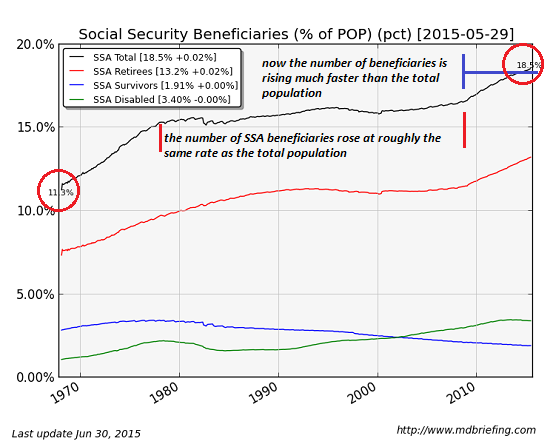

As the 60+ million baby Boom began qualifying for Social Security and Medicare entitlements, the percentage of beneficiaries rose quickly from a decades-long level of about 16% of the total population to 18.5%. This might seem like much, but what’s troubling is the steep rise in the number of beneficiaries while the number of full-time workers who pay the vast majority of the income taxes has remained stagnant:But due to demographics and a structurally stagnant economy, entitlements and pension costs are rising at a much faster rate than the revenues needed to pay the promised benefits. Two charts (courtesy of Market Daily Briefing) tell the demographic story:

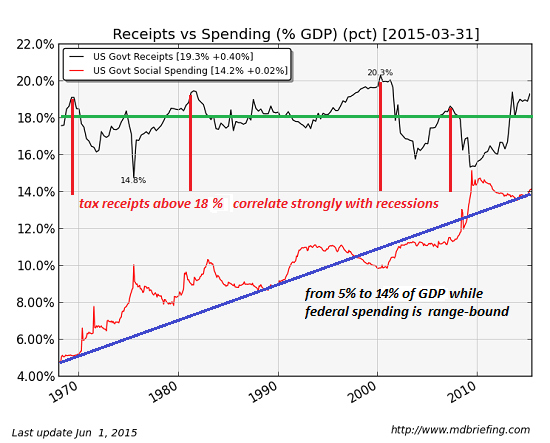

Federal social spending (entitlements) has almost tripled from 5% of GDP to 14% while federal tax revenues/spending have remained range-bound as a percentage of GDP. In other words, social spending is soaring as a percentage of the economy (GDP) while revenues to support that spending are limited by the slow-growing economy and the correlation between high tax rates and recessions.

The other structural headwind is low investment returns in a zero-interest rate global economy. The only way to increase yields is to take on more risk, a strategy that has potentially catastrophic consequences: Read the Whole Article

Leave a Reply