Keynesians Are About To Get Mugged

Yellen said at least one thing of importance last week, but not in a good way. She confessed to the frightening truth that the FOMC formulates its policies and actions based on forecasts of future economic developments.

My point is not simply that our monetary politburo couldn’t forecast its way out of a paper bag; that much they have proved in spades during their last few years of madcap money printing.

Notwithstanding the most aggressive monetary stimulus in recorded history—-84 months of ZIRP and $3.5 trillion of bond purchases—–average real GDP growth has barely amounted to 50% of the Fed’s preceding year forecast; and even that shortfall is understated owing to the BEA’s systemic suppression of the GDP deflator.

What I am getting at is that it’s inherently impossible to forecast the economic future, but that is especially true when the forecasting model is an obsolete Keynesian relic which essentially assumes a closed US economy and that balance sheets don’t matter.

Actually, balance sheets now matter more than anything else. The $225 trillion of debt weighing on the world economy——up an astonishing 5.5X in the last two decades—– imposes a stiff barrier to growth that our Keynesian monetary suzerains ignore entirely.

Likewise, the economy is now seamlessly global, meaning that everything which counts such as labor supply and wage trends, capacity utilization and investment rates and the pace of business activity and inventory stocks is planetary in nature.

By contrast, due to the narrow range of activity they capture, the BLS’ deeply flawed domestic labor statistics are nearly useless. And they are a seriously lagging indicator to boot.

Nevertheless, Yellen & Co. are obsessed with the immeasurable and largely irrelevant level of “slack” in the domestic labor market. They falsely view it as a proxy for the purported gap between potential and actual GDP. Not surprisingly, they are now under the supreme illusion that the labor slack has been largely absorbed and the output gap nearly closed.

So they are raising money market rates by a smidgeon to confirm the US economy’s strength and that the Keynesian nirvana of full employment is near at hand.

No it isn’t! These academic pettifoggers are so blinded by their tinker toy macro-model that they can’t even see the flashing red lights warning of recession just ahead.

Just consider the most recent data on wholesale sales and inventory. This sector of the domestic economy embodies the leading edge of business activity, meaning that trends in wholesale level sales and inventory stocking are advance indicators of the general macroeconomic outlook.

Needless to say, the soaring inventory-sales ratio is not a sign that “escape velocity” is just around the corner. Contrariwise, whenever the ratio has busted through 1.30X in the past, what came next was a recession.

Recessions happen on the main street economy, of course, when sales weaken and inventories build to the point where liquidation of excess stocks becomes unavoidable. Accordingly, of far greater significance than the 19 labor market graphs supposedly on Yellen’s dashboard is the unassailable fact that wholesale sales have now rolled over.

The natural market driven bounce back from the deep liquidation during the Great Recession is now over and done. Wholesale sales are down 4.5% from their June 2014 peak and have returned to September 2013 levels.

Moreover, it is also well worth noting that at the most recent October 2015 level, wholesale sales are now up at only a 1.6% annual rate from the pre-crisis peak. Surely that does not measure an economy that is healed and heading toward the promised land of full-employment.

So the false conclusion about the US economy’s strength derived from the Fed’s faulty labor market telemetry cannot be emphasized enough.

There has been no Fed driven main street recovery. Instead, the tepid business expansion after the 2009 bottom embodied nothing more than the natural regenerative impulses of our badly impaired but still functioning capitalist system. As the inventories of goods and labor that were thrown overboard during the post-crisis plunge were rebuilt, incomes recovered and the cycle of expansion paddled forward on its own motion.

But that’s now done, and the US economy stands fully exposed to the albatross of peak debt and the gale forces of global deflation. Yet as we indicated last week, the delusion that the Fed has actually been steering the main street expansion stems from the archaic jobs and unemployment rate data published by the BLS.

Consequently, it bears repeating that those metrics are derived from what is a 50 year-old factory based model of “potential GDP”; and reflect a full employment notion based on a census style count of job holders versus what was then mainly an adult male work force.

By contrast, in today’s world of global labor competition in goods, off-shored business services, episodic domestic gigs, temp agency labor delivery and Wal-Mart style labor scheduling by the hour and time of day, week, month and season the whole idea of “full employment” is a relic. And a stupid one at that.

The only common denominator left is the adult population, which numbers 255 million by headcount and 510 billion by standard work-year hours count. Over and against that, the US economy is currently utilizing about 243 billion labor hours annually according to the BLS, and that’s not the half of it.

Even as total labor hours employed by the private business economy have barely returned to 2007 levels—- and for that matter have scarcely grown at all from levels at the turn of the century—– the mix has continued to deteriorate. There is a larger share of even these flat-lining labor hours attributable to low-pay, part-time jobs than ever before.

No, this doesn’t mean that we have a 50% unemployment rate. But it does underscore the fact that in today’s world there are no “natural” or structurally fixed coefficients for withdrawal of available population hours from the labor force owing to retirement age, disability rates, election to non-monetized homemaker status, student status, or lifestyle preferences for malingering, begging, free charitable endeavors or asceticism.

Self-evidently, these decrements from the nation’s 250 billion undeployed potential labor hours are affected by tax and welfare policies, accumulated retirement savings and an endless list of cultural and psychological factors.

But they have little to do with any measurable business cycle; and they shift and morph steadily over time and in response to new technological and cultural developments. They are utterly beyond the reach of 25 basis points of interest rate shifts on the money markets.

In fact, what they are responsive to is global economic forces and the impact of debt on household spending and business cash flow allocation. As to the former, the overriding factor is the epic global commodity deflation now underway and the inexorable CapEx depression which is emerging in its wake.

Since our Keynesian central bankers have no clue that their prodigious money printing resulted in the drastic underpricing of credit and capital over the course of the past two decades, they are flying blind. They simply fail to see that the global economy is now swamped in more excess capacity than at any time since the 1930s, and probably even then.

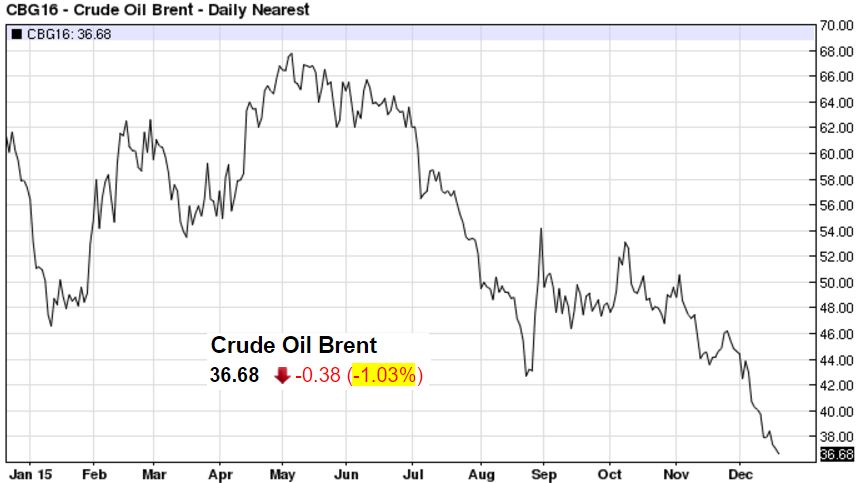

So they keep expecting the commodity cycle to momentarily bottom and prices to rebound, thereby reflating CapEx and household spending. In that context, the following chart showing how the Keynesian fellow-travelers at the IMF viewed the outlook for Brent oil prices as recently in June 2015 is dispositive.

That’s right. The least probable downside scenario was for oil above $40 per barrel through 2015. Needless to say, the Brent price has already penetrated through that level, and still has not inconsiderable downside to go—-given the rapid rate at which economic activity in China and among its EM supply chain is weakening.

In Part 2 we will further demonstrate why the labor market has become such a lagging indicator. Suffice it to say that this untoward development is mainly due to the fact that the C-suite in corporate America has been transformed into a stock trading room.

That is, it reflects a state of mind among top executives that is obsessively focused on short-run share prices and financial engineering maneuvers such as stock buybacks and M&A deals designed to goose stock prices higher, along with the value of their stock options.

Consequently, as the Fed’s serial financial bubbles rise toward their apogee, the C-suite remains inordinately bullish until the last minute, hoarding labor far longer than would otherwise be the case. Then when sales begin to visibly weaken, they liquidate payrolls with a vengeance—-that is, after the recession has already incepted.

So the unemployment rate tells you almost nothing useful. By contrast, there are an immense number of leading indicators which track the global credit bubble and false boom it enabled.

They bear far more directly and efficaciously on the main street outlook than does the Fed’s primitive bathtub model of the US economy. The latter assumes that the unemployment rate is a proxy for how close it has come to being filled to the full employment brim, but tells nothing about the leading edge global forces which drive future outcomes.

As has been widely lamented, the last stages of the US recovery in 2013-2015 have been tepid by all historic standards. Yet even these “disappointing” quarterly outcomes did not reflect Fed stimulated domestic growth, as claimed by the Keynesians.

Rather, the 2% or so GDP growth of the last several years reflects the inertial momentum in the US domestic economy that was triggered by China’s massive credit and construction spree during 2009-2013 and the upstream bow wave it generated in EM economies. But that impulse, which was driven by massive central bank enabled credit expansion, crested long ago and has now morphed into the global commodity collapse and rapid weakening of world trade.

The data on US exports of industrial supplies and materials track that cycle quite dramatically. After an initial surge that peaked in 2011-2012, these exports have plunged by nearly 40%.

The crucial point here is not that the US first gained competitive advantage in industrial materials at the end of the Great Recession, and then suddenly lost it owing the strengthening dollar. While the exchange rate effect is of some importance, what really happened is altogether different and cannot be found anywhere in the Fed’s standard Keynesian model.

To wit, the credit-driven China/EM boom sucked in scrap steel, recycled paper and cardboard, coking coal and numerous other industrial feedstocks like there was no tomorrow. While the Obama White House and Fed alike were crowing about the rebound of US exports and recapture of former competitive advantage, and Obama was projecting that a revived American export sector would double by 2015, they were actually taking credit for nothing more than the one-time evacuation of America’s scrap yards and coal mines.

Indeed, the boom even sucked out all the excess petroleum products that could be produced in the Texas and the Gulf Coast refineries. But after rising by 3X between 2008 and early 2014, even refined product exports have hit the flat-line.

US Petroleum Exports data by YCharts

More importantly, the same global dynamic applies to US exports as a whole. For instance, as the worldwide CapEx depression set-in, US exports of capital goods also peaked and are now heading south.

Thus, exports have not doubled. Not even close. In fact, total US exports of goods are now down 11% from their August 2014 peak, and in the most recent reading were only 3% above their prior peak in 2008. That’s no kind of 2X.

Nor does the argument that exports are only 12% of GDP detract from this point. What matters is trends on the margin, and they are heading south at a rapid clip in response to the onrushing global recession.

For instance, during the height of the China/EM boom and dollar weakness cycle, tourism to the US flourished like never before and by the 2014 peak was more than double its 2002 level. But the global deflation inherently means that foreign incomes are falling and the dollar’s exchange rate is rising.

Consequently, exports of travel services (i.e. tourism) have already rolled over by 7% from their early 2014 peak, and are now likely plunging much lower. That will soon become evident when punk data on X-mas sales from the ultimate tourist mecca, New York’s Fifth Avenue shopping emporiums, become available.

Don’t expect the December jobs report to capture any of this rollback in tourism and trade. The monthly numbers are so seasonally maladjusted and trend-cycle inflated that it will be years before benchmark adjustments from actual payroll tax data capture the downturn already underway.

Reprinted with permission from David Stockman’s Contra Corner.

The post Keynesians Are About To Get Mugged appeared first on LewRockwell.

Leave a Reply