The bear will soon be arriving in earnest, marauding through the canyons of Wall Street while red in tooth and claw. Our monetary central planners, of course, will once again—for the third time this century——be utterly shocked and unprepared. That’s because they have spent the better part of two decades deforming, distorting, denuding and destroying what were once serviceably free financial markets. Yet they remain as clueless as ever about the financial time bombs this inexorably fosters.

The sum and substance of Keynesian central banking are the falsifications of financial prices. In essence, this means pegging interest rates below market clearing levels on the theory that more borrowing and spending will thereby ensue.

To this traditional credit channel of monetary policy transmission has been added in recent years the notion of an FX channel, which works through currency depreciation and export stimulus; and the wealth effects channel, which seeks to levitate the paper wealth of the top 10% of households so that they will feel emboldened to spend more at luxury retail emporiums, BMW showrooms, and upscale vacation spots.

Needless to say, currency trashing might work for a tiny export economy like New Zealand. But on a global scale among the big national economies, it’s just a recipe for a race to the bottom. Ultimately it leads to nothing more than the inflation of imported commodities and goods and the reallocation of income and wealth from domestic industries and households to exporters and their shareholders. Japan proves that in spades.

With respect to the false FX channel, even Black Rock’s chief big thinker, Peter Fisher, hit the nail on the head last week on Bloomberg:

“But let’s be clear, negative rates for the FX rate is about a race to the bottom of competitive devaluation,” he asserted. “The International Monetary Fund was established to try to prevent us from doing that again, what we did in the 1920s and ’30s that were such a disaster.”

It is a measure of the political euthanasia induced into American politics by 20 years of central bank dominance that the so-called wealth effects channel is even taken seriously. It amounts to a massive fiscal transfer and trickle-upto the most affluent 10% of US households who own 85% of financial assets.

Moreover, this odious reverse robin hood feat is effected by 12 unelected apparatchiks who sit on the FOMC. From their august perches, they perform live monetary experiments on the American public with no accountability whatsoever.

That these depredations are fostering a hideously unjust redistribution of wealth from the main street to a tiny elite of money shufflers, gamblers, and silicon valley bubble-riders is attested to by the rise of Bernie Sanders, and Donald Trump, too. Besides stoking xenophobia and racial prejudice, The Donald is heading toward the GOP nomination because, ironically, he is self-funded and can loudly and honestly boast that he is not beholden to the Fat Cats who rule the country.

Besides the rank injustice, there is also the sheer stupidity of it. Implicit in the whole misbegotten wealth effects doctrine is the spurious presumption that the Wall Street gambling apparatus can be rented for a spell by the central bank. So doing, our monetary central planners believe themselves to be unleashing a virtuous circle of increased spending, income and output, and then more rounds of the same.

At length, according to these pettifoggers, production, income, and profits catch-up with the levitated prices of financial assets. Accordingly, there are no bubbles; and, instead, societal wealth continues to rise happily ever after.

Not exactly. Central bank stimulated financial asset bubbles crash. Every time.

The Fed and other practitioners of wealth effects policy do not rent the gambling apparatus of the financial markets. They become hostage to it and eventually become loathe to curtail it for fear of an open-ended hissy fit in the casino. Bernanke found that out in the spring of 2013, and Yellen three times now——in October 2014, August 2015 and January-February 2016.

But unlike the last two bubble cycles, where our monetary central planners did manage to ratchet the money market rate back up to the 6% and 5% range, by 2000 and 2007, respectively, this time, an even more obtuse posse of Keynesian true believers rode the zero bound right to the end of capitalism’s natural recovery cycle.

Accordingly, the casinos are populated with financial time bombs like never before. Worse still, the central bankers are now so utterly lost and confused that they are all thronging toward the one thing that will ignite these time bombs in a fiery denouement.

That is negative interest rates. This travesty reflects sheer irrational desperation among central bankers and their fellow travelers, and will soon illicit a fire storm of political revolt, currency hoarding and revulsion among even the gamblers inside the casino.

Besides that, they are crushing bank net interest margins, thereby imperiling the solvency of the very banking system that the central banks claim to have rescued and fixed.

We will treat with some of the time bombs set to explode in the sections below, but first it needs to be emphasized that the third bubble collapse of this century is imminent. That’s because both the global and domestic economy is cooling rapidly, meaning that recession is just around the corner.

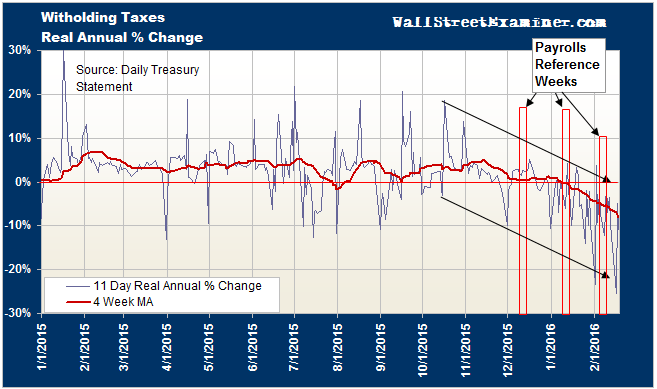

Based on the common sense proposition that the nation’s 16 million employers send payroll tax withholding monies to the IRS based on actual labor hours utilized—-and without any regard for phantom jobs embedded in such BLS fantasies as birth/death adjustments and seasonal adjustments——my colleague Lee Adler reports that inflation-adjusted collections have dropped by 7-8% from prior year in the most recent four-week rolling average.

As Lee noted in his Wall Street Examiner:

The annual rate of change in withholding taxes for collections through Thursday, February 18, approached a level which signals not just recession but is within a couple of percent of indicating a full fledged economic depression. As of February 18, 2016, the annual rate of change was -5.6% in nominal terms versus the corresponding period a year ago. That’s down from -3.7% a week before, +0.6% a month before, +5.8% three months ago, and down from a peak of +8.7% in early February 2015…….Adjusted for the nominal growth rate of employee compensation, the implied annual real rate of change is now roughly –7.5 to -8% year over year.

So there will be carnage in the casino when it becomes evident that recession has again visited this fair land, but that the Fed is utterly out of dry powder. There is not a chance in the world that NIRP will work or even be permitted by what will be the suddenly awaked politicians of Washington.

Even Peter Fisher admitted that NIRP signals the end of the road for Keynesian central bankers:

Fisher believes that central bankers’ growing penchant for negative policy rates stems from a desire to avoid admitting that they’ve expended all of their monetary ammunition.

Yet what immense societal damage these fanatics have done charging mindlessly toward this dead end. In fact, our monetary central planners have become so self-deluded and drunk with power that they now dispense sheer nonsense with complete alacrity. Thus, the Fed’s actual printing press operator, Simon Potter of the New York Fed, relieved himself of the following tommyrot in a speech today at Columbia University:

The Fed used to use a scarcity of bank reserves to set monetary policy but has had to adopt new toolsfor raising rates with a balance sheet of $4.5 trillion.

“We have achieved excellent controlover the effective federal funds rate, and we have done so while avoiding unintended effects on the financial system or financial stability,” Potter said.

Is this man kidding? There is no Federal funds market worthy of the name. The Fed’s massive bond purchasing program and the monumental excess reserves it generated obviated and destroyed the fed funds market long ago; and at a miniscule $45 billion, the residue of a market which trades virtually by appointment now amounts to just 0.3% of the footings of the US banking system.

Well, here are the Fed’s “new tools”. What they achieve is not a financial price or interest rate; what they produce is a purely counterfeit rate issuing from what amounts to a monetary circle jerk.

To wit, the Fed raised the cap on its domestic reverse repo bid from $300 billion to $2 trillion and set the yield at 25 basis points. On top of that, it has raised the foreign bank repo pool to $250 billion, where its now paying approximately 33 basis points. Finally, the interest rate it pays member banks with excess reserves (IOER) of approximately $2.5 trillion has been raised to 50 basis points.

Just call the combination of these three facilities the mother of all Big Fat Bids. And throw in the fact that the US treasury is now also flooding the market with T-bills. Under those conditions, how could it be otherwise than that money market rates, including federal funds, would settle in the FOMC’s 25-50 basis point target range?

So what? The Fed is operating a giant monetary sump pump for no rational purpose whatsoever, and it’s based on a pure financial fraud to boot.

On the former point, there is not a single rational business in America that would actually wish to fund its working capital or any other assets on an overnight tender. That’s why even floating rate revolvers have terms of a year or longer and contractual guarantees of availability if covenants are complied with.

The only beneficiaries of overnight money at 38 bps are Wall Street carry trade gamblers, and they would be just as grateful for an announced pegat 12 bps or 100 bps or even 250 bps. The only thing they really care about is short-run certainty about the cost of carrying their gambling chips—-something the Fed’s peg unfailingly provides. From the perspective of the main street economy, however, the whole federal funds targeting gambit is a thoroughly pointless farce.

So, yes, the Keynesian fools in the Eccles Building are mounting what amounts to a $6 trillion bid in order to peg with great precision a money market rate that is of absolutely no moment to the main street economy. That’s because the US household and business sectors are already at Peak Debt. Consequently, the old Keynesian credit channel of monetary policy transmission is over and done. The monetary central planners, therefore, are pushing on a credit string to no effect except to further drastically deform and destabilize a financial system that is already on the verge of implosion.

But what makes the world so dangerous is that they are doing it with a fraudulent Rube Goldberg Contraption that establishes beyond a shadow of the doubt that the FOMC is lost in a monetary puzzle palace, and is capable of virtually any kind of desperate gambit. After all, just recall where this Big Fat Bid of $6 trillion equivalent comes from.

The $2 trillion overnight reverse repo facility essentially means that the Fed is hocking a part of its massive $4.5 trillion troves of treasury bonds and mortgage-backed securities to borrow cash that it doesn’t need. And, yes, this repo collateral was previously purchased with fiat credits that it had conjured from thin air and deposited into the bank accounts of Wall Street dealers who sold these securities to the Fed’s Open Markets desk via QE.

Then again, the banking system in aggregate didn’t have an immediate need for the new reserves injected via QE so they accumulated at the New York Fed, rising from a level just $40 billion in August 2008 to $2.5 trillion at present. Now, stacked as they are in towering digital piles at 33 Liberty Street, the second component of the Feds “new tools” keeps these previously inconceivable quantities of excess reserves happily sequestered. That is, they are bribed to stay put by 50 bps of IOER payments.

There shouldn’t be any confusion here. The Fed is gratuitously subsidizing its member banks to the tune of $13 billion annually for no rational purpose whatsoever except to keep these funds from leaking into the money market and quashing its pointless fed funds target.

And the same goes for the 33 bps being earned by offshore banks which have deposited $250 billion of excess cash in the NY Fed’s foreign repo pool. Surely Deutsche Bank, Barclays, BNP Paribas and the assorted other dinosaurs of European socialism are grateful for a better return on their idle cash than the negative yield on offer from their own NIRPing central bank in Frankfurt.

Yet does this goofball Simon Potter really think that this rank outrage is a measure of the Fed’s “excellent control” over its money market targets?

And that ain’t the half of it. All the bribes being paid through these three different channels in order to peg a completely pointless target for the non-existent fed funds market reduces the Feds annual “profit”. And if the notion of profit, which lies at the very heartbeat of capitalism, ever needed to be qualified in quotation marks, this is the case.

The Fed earns revenue of approximately $120 billion per year from the $4.5 trillion troves of assets that it paid for with fictional credit rather than the proceeds of work, production and real economic value added. From that intake, it consumes $5-6 billion on its 22,000 staffers and army of contractors and consultants, many of whom otherwise pretend to teach “economics” in the nation’s colleges and universities. It now also spends upwards of $15 billion or so to pay the IOER and interest on its reverse repo borrowings and foreign bank depositors, resulting in net “profits” of about $100 billion.

This abortion of the very concept of profit is then recycled back to the US treasury as a giant bribe to keep the politicians at both ends of Pennsylvania Avenue pacified and out of its hair. Worse still, the Fed’s remanded profits are booked as an offset to the interest cost on the nation’s staggering $19 trillion of public debt, thereby enabling the politicians to believe there is a fiscal free lunch after all.

Unfortunately, all of this fraudulent monetary shuffling has a terrible consequence in the financial casinos here and aboard. It drives interest rates to sub-economic levels and triggers a massive hunt for yield among the world’s money managers and home gamers alike.

Today Bloomberg published a telling study of the baleful consequence this central bank fostered hunt for yield has had on the world’s energy and mining industries. To wit, it has enabled companies in what are highly cyclical, risky and volatile commodity industries to borrow heretofore inconceivable amounts of money, and plow it into massive malinvestments and excess capacity. As Bloomberg explained it,

One possible explanation is the level of exposure that banks and investors have to the industry. The 5,000 biggest publicly traded companies tracked by Bloomberg in the iron and steel, metals and mining, and energy sectors have a combined $3.6 trillion in debt, according to their most recent financial reports, or double what they had at the end of 2008.

Five years ago, those companies tracked by Bloomberg had more operating income than debt, on average. Now, it would take them more than eight years’ worth of current earnings, without provisioning for interest, taxes, depreciation or amortization, to clear their combined net obligations.

Yield-hungry bond investors sucked up a lot of the debt that was issued and now hold about $2.1 trillion of outstanding notes. They’ll be first to feel the pain considering Standard & Poor’s has already downgraded securities equivalent to 47 percent of that amount and made some 400 negative-ratings moves in the basic materials and energy sectors over the past 12 months alone. Such scale and depth is reminiscent of the way banks were slaughtered by ratings companies during the 2008 financial crisis.

It’s unclear where the other portion of the $3.6 trillion in liabilities lies but probably, most of it is owed to banks. If the remaining $1.5 trillion is indeed on the balance sheets of financial institutions, that would represent about 1.5 percent of the total assets of all the world’s publicly traded banks. That doesn’t seem very significant, or any cause for concern. But to put it in some context, U.S. subprime mortgages represented less than 1 percent of listed banks’ assets at the end of 2007.

Luckily, the debt of commodity companies hasn’t been repackaged into other weird and wonderful securities in the same way American home mortgages were, thus spreading the exposure. But its sheer size, and the fact such a big portion may be held by banks, suggests there’s a huge global risk here.

The bottom line is simple. The great wave of commodity and industrial deflation now sweeping through the world economy is the bastard offspring of the debt binge that was enabled by the central banks over the last two decades. Yet they now pretend that this massive headwind to growth originated in some exogenous force that must be counted with even more of the same monetary intrusion.

That’s how we get to the crime of NIRP. Keynesian central banks cannot imagine a problem for which more debt is not the solution. But is it not lack of “aggregate demand” which is idling an increasing share of the world’s oilfield drilling equipment; nor did it cause Caterpillar’s heavy mining machinery sales to plunge or the Baltic Dry index to plummet to 30-year lows.

What is driving output, wages and profits drastically southward throughout the materials and energy complex are drastically sinking profits and a desperate need to conserve cash flow in order to survive. The CapEx budget of global mining giant BHP is a proxy for what is becoming a global CapEx depression in the world’s industrial economy.

To wit, at the peak of the global credit boom and China/EM growth frenzy a few years ago, BHP’s capital budget was about $23billion. This year, by contrast, it is expected to come in at just $7billion and plunge further to only $5billion in 2017.

Needless to say, it does not take much imagination to envision how a 78% cut in capital spendingby a giant user of heavy machinery and engineered infrastructure like rail lines and port facilities will cascade down the supply chain. And since the top executives who ran these operations right over the credit bubble cliff are being fired right and left, another thing is quite certain.

That is, there are no takers for incremental debt at any price, NIRP or otherwise, in the global mining and energy industries. Epic damage has already been down, and the overhang of excess capacity and malinvestment will linger for years to come. Even then, hundreds of billions of the debt which funded this massive and mindless investment spree will be restructured or written off entirely, as is already emerging in the US shale patch.

These kinds of financial time bombs are lurking everywhere in the global economy——even if the central bankers don’t see them coming. In Part 2, we will consider the Unicorn Bubble in Silicon Valley and the tech sector, and then the ultimate detonator of the next crash—–the $3 trillion ETF bubble.

Leave a Reply