Why We’re So Risk-Averse: “We Can’t Take That Chance”

You’ve probably noticed how risk-averse Hollywood has become: the big summer movies are all extensions of existing franchises–mixing up the superheroes in new combinations, or remaking hit films from the past–all safe bets.

The trend to “playing it safe” is not limited to Hollywood:–we see risk aversion in every sphere of the economy and society.

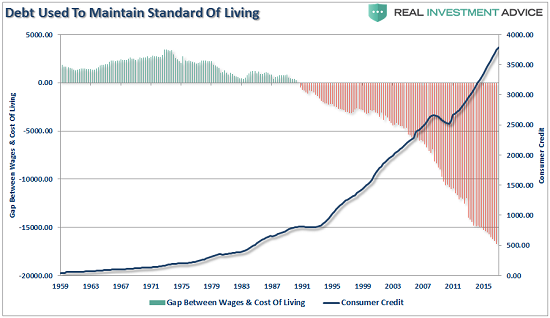

The unfailingly stimulating Ben Hunt of the Epsilon Theory newsletter has been highlighting the connection between super-easy-money financial policy and the avoidance of risk that’s so apparent in Corporate America: rather than take a chance that an investment in new technology, worker productivity etc. will increase sales and profit margins, corporations are borrowing super-cheap money and using this “nearly free money” to buy back their own shares in the stock market. ( Gradually and Then Suddenly).

This reduction of outstanding shares boosts sales and profits per share, creating higher earnings per share without actually boosting sales or profits.

Hunt’s point is that easy-money policies actually reduce the incentives to take risks to improve productivity/ profitability, and this ends up crippling our economy, as growth and productivity require taking on some risk. No risk-taking = no productivity gains and thus no gains in wealth, prosperity, social mobility, etc.

I agree with Hunt’s description of the perverse incentives created by easy-money policies, but I don’t think that’s the only driver of risk aversion, or even the primary driver.

We see this pervasive avoidance of risk in other areas as well–for example, in what college students are choosing as majors and what policy makers at the highest levels (the Federal Reserve, for example) are saying, in word and deed, “We Can’t Take That Chance.”

In the case of the Fed, the Fed is saying “We Can’t Take the Chance” that a recession would be positive, i.e. that a normal business-credit-cycle recession would do its intended job: clear out the deadwood of defaulted loans and eliminate marginal borrowers, lenders and enterprises.

This clearing of deadwood then sets the stage for healthy expansion of credit and business.

The Fed is clearly fearful that even a mild recession will cascade into something much worse–and something beyond their control.

This gives us some insight into the dynamics of risk avoidance: when we’re confident that we can handle whatever comes our way, then we’re free to take a risk on something that could yield long-lasting, important gains.

In other words, if we’re confident we can handle the downside of a risk not paying off, then we’re able to accept some risks as the necessary means of reaping major gains.

But if we’re afraid that any loss might collapse our world, then “We Can’t Take the Chance.”

Put another way–if our faith in the future and our resilience is near-zero, then we can’t take any chances. We are restricted to taking only the safest path, even if it means foregoing all the really big gains that are reserved for those willing to accept some risk.

This is an enormously important dynamic, for it hollows out the entire society and economy, one “we can’t take any chances” at a time.

One of points in this essay on Survivorship Bias is that “luck” is not just a matter of belief or some sort of magic: those who feel lucky are confident enough to absorb a wide range of contexts and opportunities. They don’t cross off most of a list, they scan it with an open mind. The lucky are lucky because they don’t arbitrarily narrow the opportunities they happen upon out of fear, i.e. we can’t take any chances.

It’s the confidence of the lucky that’s lacking in risk avoidance, and the terrible irony is avoidance of risk is also avoidance of opportunity.

There’s one more irony at work in this dynamic: as systemic risk of collapse rises, participants intuitively shun risk and start “playing it safe.” But since risk is now systemic, risk avoidance by enterprises and households won’t lower the risk of the whole rickety financial system giving way.

Rather, each individual decision of “we can’t take the chance” further weakens the economy’s resilience to financial disruption by removing the gains that are only possible by taking on risk.

Few (if any) mainstream economic pundits seem to grasp this dynamic.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

Leave a Reply