Jerome Is the New Jane

The election of 2016 was supposed to be the most disruptive break with the status quo in modern history, if ever. On the single most important decision of his tenure, however, the Donald has lined-up check-by-jowl with Barry and Dubya, too.

That is to say, Trump’s new Fed chairman, Jerome Powell, amounts to Janet Yellen in trousers and tie. In fact, you can make it a three-part composite by adding Bernanke with a full head of hair and Greenspan sans the mumble.

The overarching point here is that the great problems plaguing American society – scarcity of good jobs, punk GDP growth, faltering productivity, raging wealth mal-distribution, massive indebtedness, egregious speculative bubbles, fiscally incontinent government – are overwhelmingly caused by our rogue central bank. They are the fetid fruits of massive and sustained financial repression and falsification of the most import prices in all of capitalism – the prices of money, debt, equities and other financial assets.

Moreover, the worst of it is that the Fed is overwhelmingly the province of an unelected politburo that rules by the lights of its own Keynesian groupthink and by the hypnotic power of its Big Lie. So powerful is the latter that American democracy has meekly seconded vast, open-ended power to dominate the financial markets, and therefore the warp and woof of the nation’s $19 trillion economy, to a tiny priesthood possessing neither of the usual instruments of rule.

That is to say, never before in history has a people so completely and abjectly surrendered to an occupying power – even though its ostensibly democratic government already possessed all the votes and all the guns.

So it is no exaggeration to say, therefore, that the Fed is an alien state unto itself. That was powerfully symbolized most recently by the appointment of John Williams, a lifetime apparatchik at the San Francisco Fed, to the job of head satrap at the central bank’s Liberty Street outpost in the heart of Wall Street.

In the scheme of things, the President of the New York Fed is #2 in the whole central banking apparatus, and as such is immensely more powerful than any Senate Committee Chairman or House Speaker. But Williams’ appointment was not reviewed or passed upon by a single elected official accountable to any voter anywhere in the US of A.

Yet here is an academic scribbler so out of touch with reality that he advocates raising the Fed’s inflation target to 3% because it’s purportedly good for American workers; and who for nearly 100 months also voted to keep interest rates pinned to the zero bound even though it was crushing savers and retirees.

Worse still, Williams advanced these oppressions of the people because he claims to have espied an invisible thing called “the neutral rate” of interest that no saver or borrower in America has ever seen and that no free market would ever produce. That’s because the only true interest rate is the market rate at any given moment, not the artifacts pegged by the FOMC and the imaginary “target rate” from which they are derived.

If Dr. Williams ever had to defend slashing the purchasing power of worker paychecks, transferring wealth from retirees to the banks and worshipping a tiny interest rate number that no one can see, do we think he could get elected dog catcher, even in San Francisco?

No, we do not!

To be sure, unlike the case of the 12 regional Fed presidents, 7 of the 12 members of the ruling FOMC are appointed by the President and confirmed by the Senate. But the fact is, the Big Lie is so deeply rooted in the political system – including the GOP which is supposed to be the party of free markets and sound money – that these appointments are drawn from a narrow circle of Keynesian economists, bankers and government careerists, making the democratic review process entirely pro forma.

For crying out loud. The Donald came to Washington threatening to drain the swamp and ended up appointing to the one job that could have made a difference a crony capitalist Keynesian who was literally born and bred in the Washington DC Swamp and never left it during his entire adult life.

Needless to say, the Big Lie in question is four-fold. The central bank and its retainers and Wall Street beneficiaries claim that:

- the free market has a death wish and tends toward cyclical instability, recession and even depression without the guiding hand of the state and its central banking branch;

- when capitalism is plodding forward on its own energy during periods of business expansion, it’s the result of the Fed’s beneficent ministrations;

- when the Fed’s serial financial bubbles finally implode, the blame lies with the very speculators it enabled and financed with cheap carry trades, falling cap rates and price-keeping operations (“puts”); and

- notwithstanding the occasional externally caused financial bust, the mainstreet economy is always getting stronger and more prosperous because the FOMC is deftly guiding it to just the right balance of “full-employment” (vaguely defined as +/- 4% on the U-3 unemployment rate) and “full-inflation” (precisely defined as 2.00% on the PCE deflator – after excluding food, energy and other subjectively identified price aberrations).

It is to the latter risible narrative that we turn today in rebuke of Jerome Powell’s positively deceitful speech on “The Outlook for the US Economy” recently delivered to the Economic Club of Chicago.

According to the new Janet:

At the Federal Reserve, we seek to foster a strong economy for the benefit of individuals, families, and businesses throughout our country….After what at times has been a slow recovery from the financial crisis and the Great Recession, growth has picked up. Unemployment has fallen from 10 percent at its peak in October 2009 to 4.1 percent, the lowest level in nearly two decades. Seventeen million jobs have been created in this expansion, and the monthly pace of job growth remains more than sufficient to employ new entrants to the labor force. The labor market has been strong, and my colleagues and I on the Federal Open Market Committee (FOMC) expect it to remain strong. Inflation has continued to run below the FOMC’s 2 percent objective but we expect it to move up in coming months and to stabilize around 2 percent over the medium term.

Beyond the labor market, there are other signs of economic strength. Steady income gains, rising household wealth, and elevated consumer confidence continue to support consumer spending, which accounts for about two thirds of economic output. Business investment improved markedly last year following two subpar years, and both business surveys and profit expectations point to further gains ahead. Fiscal stimulus and continued accommodative financial conditions are supporting both household spending and business investment, while strong global growth has boosted U.S. exports.

Essentially, there is not a shred of truth in the entire passage unless you want to play 6th grade games with short-term deltas in the vaunted “incoming data”.

But apply any concept of context and notion of reasonable time duration to any of the bolded assertions and you see that Powell is either a fool or so doped-up by the Keynesian Cool Aid that he speaks jabberwocky without even knowing it.

We’d like to think it’s the latter, but anyone who starts with an assessment of the US economy by citing the 17 million jobs number is actually giving Donald Trump’s daily twitter spinning a run for the money. After all, 7 million of that number consists of born again jobs that were wiped out during the deepest recession of modern times, and have only been slowly recovered during the 9 years since.

And if you want to count from the bottom (February 2010), you will find that among the full-pay, full-time jobs in the goods-producing sector, the loss between the pre-crisis peak of 22.02 million jobs and the February 2010 bottom was 4.4 million jobs or 20% of the total.

But here’s the thing. As of last Friday’s report for March 2018, only 2.9 million or 65% of the goods-producing jobs shed during the recession have actually been recovered. The productive core of the US economy, therefore, is still 1.5 million jobs short, meaning that many of the “born again” jobs Powell was crowing about have actually been reincarnated as burger-flippers at McDonald’s and bedpan changers in the nursing homes.

Self-evidently, what our chief monetary central planner should have noted is that even on an aggregate basis – quality mix deterioration aside – the jobs market is not “strong”; it’s failing badly.

Thus, between the November 2007 cyclical peak and March 2018, the US economy generated only 9.9 million jobs. That amounts to only 80,000 per month and annualized growth rate of just 0.67%. By contrast, the adult civilian population grew by 24 million during the period or by 194,000 per month.

How this squares with Powell’s claim that “job growth remains more than sufficient to employ new entrants to the labor force” beats us, but that’s not even the most important point.

To wit, an economy lugging $68 trillion of debt, facing a baby boom retirement tsunami and heading fast towards fiscal bankruptcy needs a much stronger growth of labor input than 0.67% per year – when even that anemic growth rate was largely comprised of part-time, low productivity headcounts.

By comparison, from the June 1990 peak through the November 2007 pre-crisis peak (two full business cycles), the US economy generated 136,000 jobs per month (28.4 million total) representing an annual growth rate of 1.33%. That was double the post-crisis growth rate that Jerome was gumming about at the Chicago Economics Club.

And if you scroll back one more cycle to the June 1981-June 1990 Reagan/Bush expansion, job growth averaged 170,000 per month. Moreover, given the smaller size of the labor force back in the 1980s that computed to a 2.05% per year growth rate.

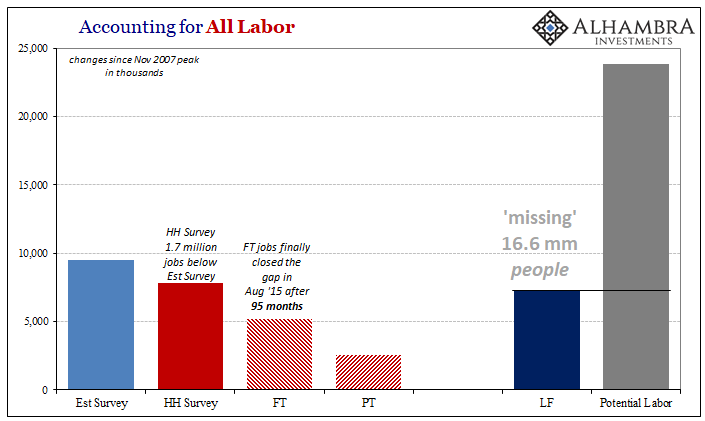

So rather than a “strong” labor market, what we really have is one that is failing miserably. As Jeffrey Snider so cogently pointed out after the March jobs report, there are actually 16.6 million “missing” workers. Indeed, after 24 million of population growth since November 2007, the US has generated only 5 million full-time jobs.

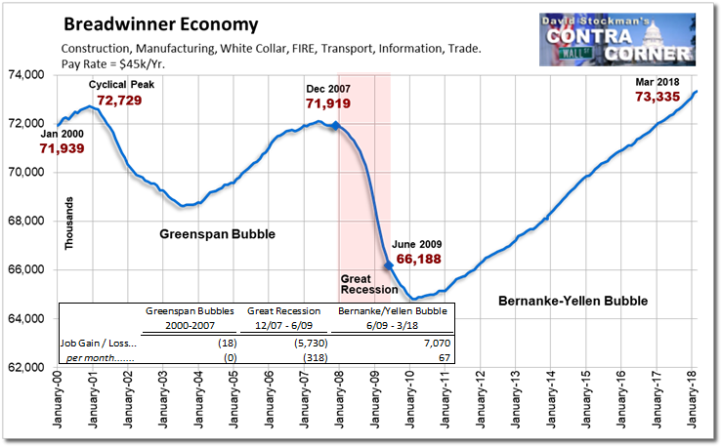

Actually, it’s worse when you look at the composition of even the 5 million “FT” (full time) jobs shown above. Since the day Bill Clinton shuffled out of the Oval Office (January 20, 2001), the US economy has generated only 606,000 new “Breadwinner” jobs. That is, full-time, full pay jobs with an ability to support a $50,000 per year wage.

Folks, if you want to call that “strong” you have apparently invented a new language because the trend gain computes to just 2,914 new Breadwinner jobs per month!

Stated differently, since January 2001 the US has generated just 15.4 million new jobs and 96% of them have been in the Part-Time Economy ( leisure, hospitality, retail, temps and other gig-oriented categories) or the HES Complex (health, education and social services).

That is to say, job growth has overwhelmingly been in the low pay and low-productivity employment that most definitely does not fuel the sustainable growth potential of the main street economy; and which also is heavily dependent upon the fiscal largesse of a government that is tumbling into fiscal collapse.

As they say on late night TV, however, that’s not all, and it’s not even the half of it. The Fed heads have been reduced to obsessing about the BLS’ virtually worthless jobs reports because the other economic indicators are even weaker on a trend basis.

For instance, manufacturing output is still well below its November 2007 level, and labor productivity has grown at barely 1.0% per annum, or less than half the 2.2% rate clocked between 1954 and the year 2000.

Then there is the risible point about an export recovery. From exactly what Powell did not say and here’s why: US exports simply made a round-trip during the global commodity mini-cycle from their mid-2014 highs to a bottom in the spring 2016 and then back essentially to where they started; and that’s notwithstanding the one-time 2016-2017 surge of credit-fueled demand emanating from the Red Ponzi that accompanied the run-up to Mr. Xi’s coronation last fall.

The truth is, exports during the most recent month were almost exactly where they were 6 years ago in September 2012, and that’s not any kind of rebound!

Finally, there is the disastrous performance of the most important economic metric of all: The rate of net investment in fixed productive assets. We do not know what Jerome has been smoking to support the claim that net investment has recovered strongly, but whatever the substance, it is clearly hallucinatory.

In fact, real net business investment was still 28% below its year 2000 level as of 2016, and last year (2017) the number (which the St. Louis Fed has not yet posted) actually went down.

Call the Powell speech what you will, but we think it’s just more jabberwocky designed to rationalize an illicit central banking regime which is rotten to the core.

Needless to say, when an unelected, all-powerful arm of the state lies to the people systematically there has got to be a con job in there somewhere.

And this time even Wall Street has lost track of the scam.

Reprinted with permission from David Stockman’s Contra Corner.

The post Jerome Is the New Jane appeared first on LewRockwell.

Leave a Reply